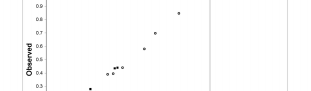

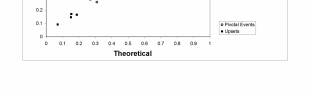

fifty elections each. The key measure of how well the theory worked is to ask how the

empirical frequency of pivotal events and upset elections compared to the prediction of

the theory. The figure above, from Levine and Palfrey [2007], plots the theoretical

predictions on the horizontal axis and the empirical frequencies on the vertical axis. It

should be emphasized that there are no free parameters – the theory is not fit to the data,

rather a direct computation is made from the parameters of the experiments. If the theory

worked perfectly the observations would align perfectly on the 45 degree line. As can be

This example of theory that works is but one of many. Other examples are double

oral auctions [Plott and Smith, 1978], and more broadly competitive environments [Roth

et al, 1991], as well as games such as best-shot [Prasnikar and Roth, 1992].

fifty elections each. The key measure of how well the theory worked is to ask how the

empirical frequency of pivotal events and upset elections compared to the prediction of

the theory. The figure above, from Levine and Palfrey [2007], plots the theoretical

predictions on the horizontal axis and the empirical frequencies on the vertical axis. It

should be emphasized that there are no free parameters – the theory is not fit to the data,

rather a direct computation is made from the parameters of the experiments. If the theory

worked perfectly the observations would align perfectly on the 45 degree line. As can be

This example of theory that works is but one of many. Other examples are double

oral auctions [Plott and Smith, 1978], and more broadly competitive environments [Roth

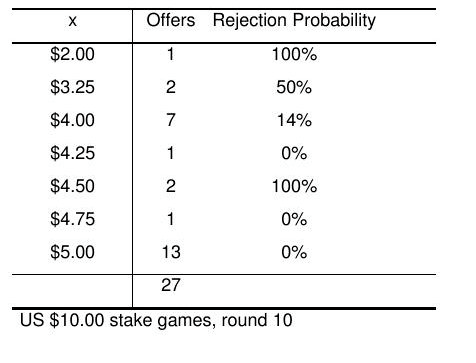

et al, 1991], as well as games such as best-shot [Prasnikar and Roth, 1992]. equilibrium must occur whatever the history of past play. In particular, in ultimatum

bargaining, if the second player is selfish, he must accept any offer that gives him more

than zero. Given this, the first player should ask for – and get – at least $9.95.

equilibrium must occur whatever the history of past play. In particular, in ultimatum

bargaining, if the second player is selfish, he must accept any offer that gives him more

than zero. Given this, the first player should ask for – and get – at least $9.95. weak compared to economic factors, but in certain types of games that may make a great

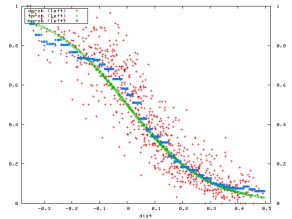

To get a sense of the limitations of existing theory, it is useful to take a look under

the hood of the voting game described above. At the aggregate level the model predicts

with a high degree of accuracy. However, as anyone who has ever looked at raw

experimental data can verify, individual play is very noisy and poorly described by the

theory. The figure below from Palfrey and Levine [2007] summarizes the play of

individuals. The optimal play for an individual depends on the probability of being

pivotal (deciding the election) and on the cost of participation. The horizontal axis

measures the loss from participating depending on the cost that is drawn. If – in the given

election – the cost drawn should make the player indifferent to participating, the loss is

zero. Otherwise it can be negative or positive, depending on how much is lost from

participating. The vertical axis is the empirical probability of participating. The red dots

are the results of individual elections. The blue dots are averages of the red dots for each

loss level, and the green curve is a theoretical construct described below. The theory says

that this “best response” function should be flat with the probability of participating equal

to one until gains (negative losses) reach zero on the horizontal axis, then a vertical line,

then again flat with a value of zero for all losses that are bigger than zero. This is far from

the case: some players make positive errors, some make negative errors. The key is that

in this voting game, the errors tend to offset each other. Over voting by one voter causes

other voters to want to under vote, so aggregate behavior is not much effected by the fact

that individuals are not behaving exactly as the theory predicts. A similar statement can

be made about a competitive auction and other games in which equilibrium is strong and

robust. By way of contrast, in ultimatum bargaining, a few players rejecting bad offers

changes the incentives of those making offers, so that they will wish to make lower offers

– moving away from the subgame perfect equilibrium, not towards it.

weak compared to economic factors, but in certain types of games that may make a great

To get a sense of the limitations of existing theory, it is useful to take a look under

the hood of the voting game described above. At the aggregate level the model predicts

with a high degree of accuracy. However, as anyone who has ever looked at raw

experimental data can verify, individual play is very noisy and poorly described by the

theory. The figure below from Palfrey and Levine [2007] summarizes the play of

individuals. The optimal play for an individual depends on the probability of being

pivotal (deciding the election) and on the cost of participation. The horizontal axis

measures the loss from participating depending on the cost that is drawn. If – in the given

election – the cost drawn should make the player indifferent to participating, the loss is

zero. Otherwise it can be negative or positive, depending on how much is lost from

participating. The vertical axis is the empirical probability of participating. The red dots

are the results of individual elections. The blue dots are averages of the red dots for each

loss level, and the green curve is a theoretical construct described below. The theory says

that this “best response” function should be flat with the probability of participating equal

to one until gains (negative losses) reach zero on the horizontal axis, then a vertical line,

then again flat with a value of zero for all losses that are bigger than zero. This is far from

the case: some players make positive errors, some make negative errors. The key is that

in this voting game, the errors tend to offset each other. Over voting by one voter causes

other voters to want to under vote, so aggregate behavior is not much effected by the fact

that individuals are not behaving exactly as the theory predicts. A similar statement can

be made about a competitive auction and other games in which equilibrium is strong and

robust. By way of contrast, in ultimatum bargaining, a few players rejecting bad offers

changes the incentives of those making offers, so that they will wish to make lower offers

– moving away from the subgame perfect equilibrium, not towards it.Microsoft word - pompa diamagnetica ctu 16 per depliant.doc

Approfondimento tecnico del dott. Tommaso Ferretti - relatore sulla tecnica diamagnetica al XXII congressonazionale ANASMED di medicina dello sport di Vittorio Veneto del 18-21 giugno 2006- POMPA DIAMAGNETICA SISTEMA INTEGRATO DI EROGAZIONE DI ENERGIA Premesse Nei confronti di un campo magnetico la materia ha, a seconda della sua composizione, tre comportamenti. Se ha proprietà