La tétracycline, connue sous le nom commercial Sumycin, agit en bloquant la fixation de l’ARNt sur la sous-unité 30S ribosomale, interrompant l’élongation de la chaîne protéique bactérienne. Ce mécanisme confère une activité sur un spectre large, incluant bactéries Gram positives, Gram négatives, rickettsies et spirochètes. Sa biodisponibilité digestive varie selon la prise alimentaire et les interactions avec les ions divalents comme calcium et magnésium. Sa diffusion tissulaire est importante, notamment dans les voies respiratoires et génito-urinaires. L’élimination se fait par voie rénale et biliaire. Les effets indésirables incluent photosensibilisation, troubles digestifs et coloration dentaire en cas d’administration précoce. Les guides thérapeutiques mentionnent sumycin prix, en soulignant la nécessité de restreindre son utilisation afin de limiter les résistances acquises.

M O R G A N S T A N L E Y R E S E A R C H N O R T H A M E R I C A Morgan Stanley & Co. LLC David Friedman, M.D. David.Friedman@morganstanley.com +1 212 761 4217 Marshall Urist, M.D., Ph.D. Sara Slifka Sara.Slifka@morganstanley.com +1 212 761 3920 Brienne Kugler Brienne.Kugler@morganstanley.com Ironwood Overweight Pharmaceuticals, Inc. Key Ratios and Statistics Reuters: IRWD.O Bloomberg: IRWD US Biotechnology / United States of America Price target We are updating our IMS TRx analysis which we first published (11/20/12) pre-Linzess launch. We believe the launch has been strong to date.

Fiscal Year ending We are updating our IMS TRx analysis which shows ModelWare EPS ($) our estimate of the TRx ramp necessary to meet our Prior ModelWare EPS ($) and (Forest) consensus US Linzess estimates from 2013-2016 (Ex. 1-3). Below, we highlight some key Consensus EPS ($)§

points of our analysis and the launch to date.

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare

Launch is Strong: We believe that the Linzess launch,

framework (please see explanation later in this note). § = Consensus data is provided by Thomson Reuters Estimates.

based on a few key metrics, has been strong to date.

e = Morgan Stanley Research estimates A) There have been ~575 TRx’s added per wk on avg.

since leaving the holiday period (Ex. 2, starting with

1/11/13 wk which is the first one post holidays). This avg 1) has held over the most recent month as well, 2) has been augmented with recent wk over wk TRx gains topping 700 TRx, and 3) is slightly ahead of our expected, above consensus 525-550 wkly 2013 TRx adds (minimally changed from prior analysis). B) Our modified slope analysis (Ex. 4), which evaluates the magnitude of TRx’s and the growth trends, signals a trajectory that still reflects an initial rapid growth phase, despite being a few months into the launch. C) Our analysis of Linzess and Amitiza TRx suggests that the Linzess launch has led to IBS-C/CC mkt expansion (Ex. 4). Given that Amitiza TRx are roughly flat, we see all of this growth (and currently ~20% share of the wkly TRx) are attributable to Linzess. 11/20/12 Analysis: We performed a similar analysis pre-launch, which despite two important changes below yielded similarly positive conclusions. The two changes are a) a lower price per TRx, in line with management’s comments implying a >15% gross to net rebate vs. our previously assumed 10%, and b) a slower ramp around

Morgan Stanley does and seeks to do business with

the 2012 holiday/new year time (we used the actual IMS

companies covered in Morgan Stanley Research. As

TRx’s from that period). To the second change, given

a result, investors should be aware that the firm may

have a conflict of interest that could affect the

that a) all wks of this type of analysis build/compound off

objectivity of Morgan Stanley Research. Investors

of the initial ones and b) our original analysis did not

should consider Morgan Stanley Research as only a

include typical holiday slowness, we wanted to re-set

single factor in making their investment decision.

our initial ests., which we view as fair.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc. IMS Methodology and Assumptions: FRX Consensus vs. MS Estimates 2013-2016

1) We have chosen to use FRX analyst estimates for our

consensus modeling as our source for consensus numbers

Forest Consensus

(Thomson) appears to have a more reliable (only including US

Revenue (000's) $106,747

revenue) and robust (many more analysts included) consensus

Morgan Stanley Revenue (000's) $138,546

2) We model Linzess actual TRx numbers through early

January 2013 in the Morgan Stanley and consensus launch to

Forest Consensus 1,472,032 Revenue (000's) $270,874

3) We model a linear ramp in ’13 and beyond. Most primary

Morgan Stanley

care drug launches have tended to be relatively linear in terms

2,187,069 Revenue (000's) $402,450

of their initial IMS ramp. For simplicities sake, we have

assumed a linear launch in our quarterly projections, adding an

Forest Consensus

equal number of prescriptions per week on top of the prior

2,134,331 Revenue (000's) $404,528 Morgan Stanley

4) We use a price per prescription of ~$179 ($7.10/day with a

3,489,583 Revenue (000's) $661,394

17.5% gross to net discount) in 2012 and 2013 with 3% per year price increases thereafter. This is below Amitiza’s monthly

2016 Forest Consensus 3,588,004 Revenue (000's) $700,449 Morgan Stanley 4,697,593 Revenue (000's) $917,063

Source: Company Data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 2 Linzess Prescription Ramp: TOP) Progress to Date vs. MS and Consensus (Zelnorm is a comparator) BOTTOM) MS vs Consensus through 2013 (Zelnorm is a comparator) ns o ti 5,000 Weekl 2,000 Week of Launch criptions Week of Launch

Source: Company Data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 3 2013-2016 IMS Forecast – MS vs. Consensus Labeling on graphs highlight Zelnorm data points that help explain TRx trajectory over time Year markers on top of graph are for Linzess related estimates (not Zelnorm) tions rip Week of Launch

Source: Company Data, Morgan Stanley Research

Exhibit 4 Linzess Modified Slope Ramp Appears Strong This analysis was performed by calculating the slope of the line that connects baseline (launch-time) to each week’s TRx level. As the TRx growth tapers down, the line connecting it to baseline is shallower (i.e. lower slope). This modified slope line is impacted by the absolute TRx level as well as the trajectory of the IMS curve. rescr P y 150 ekl e W 100

Source: Company Data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 5 Amitiza Prescriptions Have Been Stable, Market Seems to be Growing cription

Source: Company Data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc. Risk-Reward Snapshot: Ironwood Pharmaceuticals (IRWD, OW, PT $21) Linzess Success Drives Risk Reward Investment Thesis

potential. Linzess is a first-in-class GC-C (guanylate cyclase type-C)

$21.00 (+14%) We model peak WW sales of ~$2bn, and believe the stock is pricing in peak sales lower than that.

Linzess’ advantages are its strong

pain, with relatively limited side effects

Current Stock PriceWARNINGDONOTEDIT_RRS4RL~IRWD.O~

Source: Thomson Reuters, Morgan Stanley Research

Our $21 price target is derived from a discounted cash flow analysis using a WACC of 10% and a terminal growth rate of 0% post 2029. The revenue driver in

Linzess becomes dominant player in IBS and CC markets.

Linzess becomes a preferred treatment in both IBS

key difference from our base case is greater penetration into the

chronic constipation market, which will likely be the more difficult

market as CC patients tend to have milder disease than IBS (pain

is defining characteristic of IBS-C). This scenario assumes rapid adoption by physicians, no reimbursement issues, and that

hundreds of thousands of patients who deemed themselves

Linzess’ cost is a concern as the CC

previously satisfied with current treatment decide to switch

therapies due to a potentially even better benefit with Linzess.

Linzess becomes a notable player in IBS market, but less so in

competitive cost/benefit profile and use

CC. Linzess takes meaningful share of the IBS market, but gains

<20% of the Linzess eligible CC patients. We expect the CC market

to be more difficult to penetrate as the disease is less urgent for

many. Nevertheless, we expect Linzess’ profile will help it gain

enough uptake to reach ~$2bn peak sales globally. This scenario

Risks to our price target

also assumes that cost and reimbursement is not a significant issue for most patients, and a proportion of patients previously relatively

Linzess could fail to meet our sales

satisfied on laxatives decide to switch to Linzess for a potentially

Linzess falters commercially. This scenario assume Linzess

struggles to gain significant uptake due to physician hesitancy to

adopt a novel agent or reimbursement issues. Patient awareness

remains limited and there are few patients that switch from laxatives to Linzess.

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc. Valuation and Catalysts

Exhibit 5 DCF Drives Valuation

Source: Company data, Morgan Stanley Research

Exhibit 6

of Ironwood’s pipeline is relatively early-stage, thus

DCF Valuation Supports Upside to Stock Price

Linzess-independent longer-term growth is uncertain.

Valuation Date Discount Rate Revenue The revenue driver in our model is the launch of Linzess. Economics: Ironwood has partnerships in place in the US

(Forest: 50/50 profit split), EU (Almirall; royalty where Ironwood has stated the terms approach ~50% of the profits

assuming modest sales) and most of Asia (Astellas: we estimate royalty of high-teens/low 20s). COGS: We expect Linzess, a pill, will have “pharmaceutical-like” margins of >90%. Equity Value Operating Expenses: Equity Value/Sh R&D: We expect R&D will decline modestly in the near-term as

Source: Company data, Morgan Stanley Research

SG&A: We expect SG&A will remain relatively stable

near-term as Ironwood works to sell/market Linzess. Over

$21 PT includes Linzess Launch

time, we expect SG&A to decline modestly as the company

We derive our PT from a discounted cash flow (DCF) analysis

using a WACC of 10% and a terminal growth rate of 0% post

Collaboration Expense: Forest will staff ~1,400 primary care

2029. We incorporate the cash cost of stock options.

sales reps and Ironwood will build its own ~150 patient GI physician focused sales force. Ironwood splits all salesforce

Valuation Methodology: We use DCF to value Ironwood as

and marketing costs with Forest 50/50. Given the significant

well as most other companies under coverage. We believe

spending needed to build a strong primary care salesforce, we

DCF best captures the longer term nature of drug development

expect these companies will take a loss on Linzess in the first

and commercialization. We do not feel that a multiples

year of launch. This loss is accounted for in collaboration

analysis accomplishes the same goal, as it only evaluates a

Financings: We do not model any future financings for Discount Rate: We typically apply a discount rate of 10% to Risks to our price target include: Linzess could fail to gain Terminal Growth Rate: We model a 0% terminal growth rate

post-2029 after a steep decline in cash flows in 2026 as Linzess’ composition of matter patent expires in 2025. The rest

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 7 Upcoming Catalysts Expected Timing

Source: Company Data, Morgan Stanley Research

Exhibit 8 Changes to Model 2014E 2015E 2016E 2017E 2018E 2019E 2020E Comments Linaclotide US Sales ($mn) Linaclotide ex-US Sales ($mn) Linaclotide US Profit Split ($mn) Total Revenues ($mn) COGS ($mn) R&D ($mn) -ex-ESOs SG&A ($mn) - ex-ESOs Interest and Other Income, net Net Income ($MM) - Non GAAP, excludes options EPS Non-GAAP, Diluted, excludes options EPS - GAAP (Diluted) Basic Shares Outstanding Dilluted Shares Outstanding

Source: Company data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 9 Quarterly Income Statement Revenue to IRWD: Linaclotide US Profit Split Operating Expenses: Cost of Sales Operating Income (Loss)

Other Expense / Forward Purchase Contracts Pretax Income (Loss)

Provision for Income Taxes / Benefit Effective tax rate Net Loss pre MI Net Loss attributed to minority interest Net Income (Loss)

Tax benefit from optionsNet Income (excl one-time items)

Non-GAAP, diluted (inc. ESOs) GAAP EPS, diluted (inc. options expense)

Source: Company data, Morgan Stanley Research estimates

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 10 Annual Income Statement ($ in millions except per share data)

913.69 1,161.83 1,402.39 1,616.11 1,778.28

780.08 1,123.87 1,473.20 1,802.15 2,026.78 2,197.65

Revenue to IRWD: Collaboration Revenue (Linaclotide US Profit Split)

Collaboration Revenue (upfront & milestones)

$132.51 $268.24 $380.73 $518.20 $649.77 $745.79 $817.79

Operating Expenses: COGS Total Operating Expenses Operating Income (Loss)

Other Income / Forward Purchase Contracts

Pretax Income (Loss)

($53.12) ($55.05) ($219.71) ($105.78) $29.41

Net Income (Loss) Net Income (Loss) to Ironwood Pharma Non-GAAP, diluted (inc. ESOs) GAAP EPS, diluted (including ESOs)

Source: Company data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 11 Balance Sheet

Prepaid expenses & other current assets

Current assets of discontinued operations Total Current Assets 1,315.99 1,947.37

Long-term assets of discontinued operations Total Assets

Current portion of capital lease obligations

Current liabilities of discont operations

Total Current Liabilities

Long-term liabilities of discont operations

Total Liabilities

(432.39) (505.02) (742.80) (865.60) (856.62) (731.68) (464.77) (57.00)

Noncontrol ing Interest Total stockholders' equity Total liabilities and stockholders' equity

Source: Company data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Exhibit 12 Cash Flow Statement

Income (loss) from discontinued operations

Income / (Loss) from continuing operations

Loss (gain) on disposal of property and equipment

Remeasurement of forward purchase contracts

Accretion of discount / premium on investment securities

Changes in operating assets liabilities: Accounts receivable

Prepaid expenses and other current assets

Deferred rent & Capital Lease Obligations

Net cashed used in operating activities from disc ops

Net cash used in operating activities Investing Activities: Purchases of available-for-sale securities

Sales and maturities of available-for-sale securities

Proceeds from the sale of property and equipment / subsidi

Net cashed used in investing activities from disc ops

Financing activities: Proceeds from issuance of preferred stock, net of issuance costs Proceeds from share issuance

Proceeds from exercise of stock options, stock purchase pl

Proceeds from sale of noncotrolling interest in subsidiary

Disbursements from repurchase of common stock

Payments on borrowings and capital lease obligations

Net cash (used in) provided by fin activities from disc ops

Net cash provided by financing activities

Cash and equivalents at beginning of year

Source: Company data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc. Morgan Stanley ModelWare is a proprietary analytic framework that helps clients uncover value, adjusting for distortions and ambiguities created by local accounting regulations. For example, ModelWare EPS adjusts for one-time events, capitalizes operating leases (where their use is significant), and converts inventory from LIFO costing to a FIFO basis. ModelWare also emphasizes the separation of operating performance of a company

from its financing for a more complete view of how a company generates earnings.

Disclosure Section

The information and opinions in Morgan Stanley Research were prepared by Morgan Stanley & Co. LLC, and/or Morgan Stanley C.T.V.M. S.A., and/or

Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V. As used in this disclosure section, "Morgan Stanley" includes Morgan Stanley & Co. LLC,

Morgan Stanley C.T.V.M. S.A., Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V. and their affiliates as necessary.

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan

Stanley Research Disclosure Website at www.morganstanley.com/researchdisclosures, or contact your investment representative or Morgan Stanley

Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any price targets referenced in this research report, please email

morganstanley.research@morganstanley.com with a request for valuation methodology and risks on a particular stock or contact your investment

representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA. Analyst Certification

The following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and

that they have not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this

Unless otherwise stated, the individuals listed on the cover page of this report are research analysts. Global Research Conflict Management Policy

Morgan Stanley Research has been published in accordance with our conflict management policy, which is available at

www.morganstanley.com/institutional/research/conflictpolicies. Important US Regulatory Disclosures on Subject Companies

As of February 28, 2013, Morgan Stanley beneficially owned 1% or more of a class of common equity securities of the following companies covered in

Morgan Stanley Research: Auxilium Pharmaceuticals, Ironwood Pharmaceuticals, Inc., NPS Pharmaceuticals.

Within the last 12 months, Morgan Stanley managed or co-managed a public offering (or 144A offering) of securities of Amgen Inc., Celgene Corp,

Elan Corporation PLC, Immunogen Inc., Infinity Pharmaceuticals Inc, Synageva Biopharma Corp, Tesaro Inc.

Within the last 12 months, Morgan Stanley has received compensation for investment banking services from Amgen Inc., Biogen Idec Inc., Celgene

Corp, Cubist Pharmaceuticals Inc., Elan Corporation PLC, Immunogen Inc., Infinity Pharmaceuticals Inc, Ironwood Pharmaceuticals, Inc.,

Synageva Biopharma Corp, Tesaro Inc., Vertex Pharmaceuticals.

In the next 3 months, Morgan Stanley expects to receive or intends to seek compensation for investment banking services from Alexion

Pharmaceuticals, Amgen Inc., Auxilium Pharmaceuticals, Aveo Pharmaceuticals, Biogen Idec Inc., Celgene Corp, Cubist Pharmaceuticals Inc., Elan

Corporation PLC, Gilead Sciences Inc., Idenix Pharmaceuticals, Inc., Immunogen Inc., Incyte Corporation, Infinity Pharmaceuticals Inc, Ironwood Pharmaceuticals, Inc., Lexicon Pharmaceuticals, Inc., Neurocrine Biosciences Inc, NPS Pharmaceuticals, Onyx Pharmaceuticals Inc., Synageva

Biopharma Corp, Tesaro Inc., Theravance Inc, Vertex Pharmaceuticals, XenoPort Inc.

Within the last 12 months, Morgan Stanley has received compensation for products and services other than investment banking services from Amgen

Inc., Biogen Idec Inc., Celgene Corp, Cubist Pharmaceuticals Inc., Elan Corporation PLC, Gilead Sciences Inc., Vertex Pharmaceuticals.

Within the last 12 months, Morgan Stanley has provided or is providing investment banking services to, or has an investment banking client

relationship with, the following company: Alexion Pharmaceuticals, Amgen Inc., Auxilium Pharmaceuticals, Aveo Pharmaceuticals, Biogen Idec Inc.,

Celgene Corp, Cubist Pharmaceuticals Inc., Elan Corporation PLC, Gilead Sciences Inc., Idenix Pharmaceuticals, Inc., Immunogen Inc., Incyte

Corporation, Infinity Pharmaceuticals Inc, Ironwood Pharmaceuticals, Inc., Lexicon Pharmaceuticals, Inc., Neurocrine Biosciences Inc, NPS

Pharmaceuticals, Onyx Pharmaceuticals Inc., Synageva Biopharma Corp, Tesaro Inc., Theravance Inc, Vertex Pharmaceuticals, XenoPort Inc.

Within the last 12 months, Morgan Stanley has either provided or is providing non-investment banking, securities-related services to and/or in the past

has entered into an agreement to provide services or has a client relationship with the following company: Amgen Inc., Biogen Idec Inc., Celgene Corp,

Cubist Pharmaceuticals Inc., Elan Corporation PLC, Gilead Sciences Inc., InterMune, Onyx Pharmaceuticals Inc., Vertex Pharmaceuticals.

Morgan Stanley & Co. LLC makes a market in the securities of Alexion Pharmaceuticals, AMAG Pharmaceuticals, Inc., Amgen Inc., Auxilium

Pharmaceuticals, Aveo Pharmaceuticals, Biogen Idec Inc., Celgene Corp, Cubist Pharmaceuticals Inc., Elan Corporation PLC, Gilead Sciences Inc.,

Idenix Pharmaceuticals, Inc., Immunogen Inc., Incyte Corporation, Infinity Pharmaceuticals Inc, InterMune, Ironwood Pharmaceuticals, Inc.,

Lexicon Pharmaceuticals, Inc., Neurocrine Biosciences Inc, NPS Pharmaceuticals, Onyx Pharmaceuticals Inc., Optimer Pharmaceuticals, Synageva

Biopharma Corp, Tesaro Inc., Theravance Inc, Vertex Pharmaceuticals, XenoPort Inc.

The equity research analysts or strategists principally responsible for the preparation of Morgan Stanley Research have received compensation based

upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment

Morgan Stanley and its affiliates do business that relates to companies/instruments covered in Morgan Stanley Research, including market making,

providing liquidity and specialized trading, risk arbitrage and other proprietary trading, fund management, commercial banking, extension of credit,

investment services and investment banking. Morgan Stanley sells to and buys from customers the securities/instruments of companies covered in

Morgan Stanley Research on a principal basis. Morgan Stanley may have a position in the debt of the Company or instruments discussed in this report.

Certain disclosures listed above are also for compliance with applicable regulations in non-US jurisdictions. STOCK RATINGS

Morgan Stanley uses a relative rating system using terms such as Overweight, Equal-weight, Not-Rated or Underweight (see definitions below).

Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the

equivalent of buy, hold and sell. Investors should carefully read the definitions of all ratings used in Morgan Stanley Research. In addition, since

Morgan Stanley Research contains more complete information concerning the analyst's views, investors should carefully read Morgan Stanley

Research, in its entirety, and not infer the contents from the rating alone. In any case, ratings (or research) should not be used or relied upon as

investment advice. An investor's decision to buy or sell a stock should depend on individual circumstances (such as the investor's existing holdings)

and other considerations. Global Stock Ratings Distribution (as of February 28, 2013) M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

For disclosure purposes only (in accordance with NASD and NYSE requirements), we include the category headings of Buy, Hold, and Sell alongside

our ratings of Overweight, Equal-weight, Not-Rated and Underweight. Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we

cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold, and sell but represent recommended relative

weightings (see definitions below). To satisfy regulatory requirements, we correspond Overweight, our most positive stock rating, with a buy

recommendation; we correspond Equal-weight and Not-Rated to hold and Underweight to sell recommendations, respectively.

Overweight/Buy Equal-weight/Hold Not-Rated/Hold Underweight/Sell

Data include common stock and ADRs currently assigned ratings. An investor's decision to buy or sell a stock should depend on individual

circumstances (such as the investor's existing holdings) and other considerations. Investment Banking Clients are companies from whom Morgan

Stanley received investment banking compensation in the last 12 months. Analyst Stock Ratings

Overweight (O). The stock's total return is expected to exceed the average total return of the analyst's industry (or industry team's) coverage universe,

on a risk-adjusted basis, over the next 12-18 months.

Equal-weight (E). The stock's total return is expected to be in line with the average total return of the analyst's industry (or industry team's) coverage

universe, on a risk-adjusted basis, over the next 12-18 months.

Not-Rated (NR). Currently the analyst does not have adequate conviction about the stock's total return relative to the average total return of the

analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

Underweight (U). The stock's total return is expected to be below the average total return of the analyst's industry (or industry team's) coverage

universe, on a risk-adjusted basis, over the next 12-18 months.

Unless otherwise specified, the time frame for price targets included in Morgan Stanley Research is 12 to 18 months. Analyst Industry Views

Attractive (A): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be attractive vs. the

relevant broad market benchmark, as indicated below.

In-Line (I): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be in line with the relevant

broad market benchmark, as indicated below.

Cautious (C): The analyst views the performance of his or her industry coverage universe over the next 12-18 months with caution vs. the relevant

broad market benchmark, as indicated below.

Benchmarks for each region are as follows: North America - S&P 500; Latin America - relevant MSCI country index or MSCI Latin America Index;

Europe - MSCI Europe; Japan - TOPIX; Asia - relevant MSCI country index.

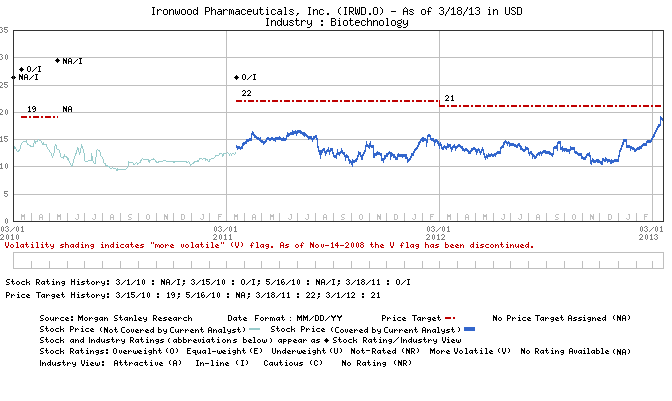

. Stock Price, Price Target and Rating History (See Rating Definitions) M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc. Important Disclosures for Morgan Stanley Smith Barney LLC Customers

Citi Research publications may be available about the companies or topics that are the subject of Morgan Stanley Research. Ask your Financial Advisor or use Research

Center to view any available Citi Research publications in addition to Morgan Stanley research reports. Important disclosures regarding the relationship between the companies that are the subject of Morgan Stanley Research and Morgan Stanley Smith Barney LLC, Morgan

Stanley and Citigroup Global Markets Inc. or any of their affiliates, are available on the Morgan Stanley Smith Barney disclosure website at

www.morganstanleysmithbarney.com/researchdisclosures. For Morgan Stanley and Citigroup Global Markets, Inc. specific disclosures, you may refer to www.morganstanley.com/researchdisclosures and

https://www.citigroupgeo.com/geopublic/Disclosures/index_a.html. Each Morgan Stanley Equity Research report is reviewed and approved on behalf of Morgan Stanley Smith Barney LLC. This review and approval is conducted by the

same person who reviews the Equity Research report on behalf of Morgan Stanley. This could create a conflict of interest. Other Important Disclosures

Morgan Stanley & Co. International PLC and its affiliates have a significant financial interest in the debt securities of Amgen Inc., Biogen Idec Inc., Celgene Corp, Cubist

Pharmaceuticals Inc., Gilead Sciences Inc. Morgan Stanley is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of

Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. Morgan Stanley produces an equity research product called a "Tactical Idea." Views contained in a "Tactical Idea" on a particular stock may be contrary to the

recommendations or views expressed in research on the same stock. This may be the result of differing time horizons, methodologies, market events, or other factors. For

all research available on a particular stock, please contact your sales representative or go to Client Link at www.morganstanley.com. Morgan Stanley Research does not provide individually tailored investment advice. Morgan Stanley Research has been prepared without regard to the circumstances and

objectives of those who receive it. Morgan Stanley recommends that investors independently evaluate particular investments and strategies, and encourages investors to

seek the advice of a financial adviser. The appropriateness of an investment or strategy will depend on an investor's circumstances and objectives. The securities,

instruments, or strategies discussed in Morgan Stanley Research may not be suitable for all investors, and certain investors may not be eligible to purchase or participate in

some or all of them. Morgan Stanley Research is not an offer to buy or sell any security/instrument or to participate in any trading strategy. The value of and income from

your investments may vary because of changes in interest rates, foreign exchange rates, default rates, prepayment rates, securities/instruments prices, market indexes,

operational or financial conditions of companies or other factors. There may be time limitations on the exercise of options or other rights in securities/instruments

transactions. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. If

provided, and unless otherwise stated, the closing price on the cover page is that of the primary exchange for the subject company's securities/instruments. The fixed income research analysts, strategists or economists principally responsible for the preparation of Morgan Stanley Research have received compensation based

upon various factors, including quality, accuracy and value of research, firm profitability or revenues (which include fixed income trading and capital markets profitability or

revenues), client feedback and competitive factors. Fixed Income Research analysts', strategists' or economists' compensation is not linked to investment banking or capital

markets transactions performed by Morgan Stanley or the profitability or revenues of particular trading desks. Morgan Stanley Research is not an offer to buy or sell or the solicitation of an offer to buy or sell any security/instrument or to participate in any particular trading strategy.

The "Important US Regulatory Disclosures on Subject Companies" section in Morgan Stanley Research lists all companies mentioned where Morgan Stanley owns 1% or

more of a class of common equity securities of the companies. For all other companies mentioned in Morgan Stanley Research, Morgan Stanley may have an investment

of less than 1% in securities/instruments or derivatives of securities/instruments of companies and may trade them in ways different from those discussed in Morgan Stanley

Research. Employees of Morgan Stanley not involved in the preparation of Morgan Stanley Research may have investments in securities/instruments or derivatives of

securities/instruments of companies mentioned and may trade them in ways different from those discussed in Morgan Stanley Research. Derivatives may be issued by

Morgan Stanley or associated persons. With the exception of information regarding Morgan Stanley, Morgan Stanley Research is based on public information. Morgan Stanley makes every effort to use reliable,

comprehensive information, but we make no representation that it is accurate or complete. We have no obligation to tell you when opinions or information in Morgan Stanley

M O R G A N S T A N L E Y R E S E A R C H March 19, 2013 Ironwood Pharmaceuticals, Inc.

Research change apart from when we intend to discontinue equity research coverage of a subject company. Facts and views presented in Morgan Stanley Research have

not been reviewed by, and may not reflect information known to, professionals in other Morgan Stanley business areas, including investment banking personnel. Morgan Stanley Research personnel may participate in company events such as site visits and are generally prohibited from accepting payment by the company of

associated expenses unless pre-approved by authorized members of Research management. Morgan Stanley may make investment decisions or take proprietary positions that are inconsistent with the recommendations or views in this report. To our readers in Taiwan: Information on securities/instruments that trade in Taiwan is distributed by Morgan Stanley Taiwan Limited ("MSTL"). Such information is for your

reference only. Information on any securities/instruments issued by a company owned by the government of or incorporated in the PRC and listed in on the Stock Exchange

of Hong Kong ("SEHK"), namely the H-shares, including the component company stocks of the Stock Exchange of Hong Kong ("SEHK")'s Hang Seng China Enterprise

Index is distributed only to Taiwan Securities Investment Trust Enterprises ("SITE"). The reader should independently evaluate the investment risks and is solely

responsible for their investment decisions. Morgan Stanley Research may not be distributed to the public media or quoted or used by the public media without the express

written consent of Morgan Stanley. To our readers in Hong Kong: Information is distributed in Hong Kong by and on behalf of, and is attributable to, Morgan Stanley Asia

Limited as part of its regulated activities in Hong Kong. If you have any queries concerning Morgan Stanley Research, please contact our Hong Kong sales representatives.

Information on securities/instruments that do not trade in Taiwan is for informational purposes only and is not to be construed as a recommendation or a solicitation to trade

in such securities/instruments. MSTL may not execute transactions for clients in these securities/instruments. Morgan Stanley is not incorporated under PRC law and the research in relation to this report is conducted outside the PRC. Morgan Stanley Research does not constitute

an offer to sell or the solicitation of an offer to buy any securities in the PRC. PRC investors shall have the relevant qualifications to invest in such securities and shall be

responsible for obtaining all relevant approvals, licenses, verifications and/or registrations from the relevant governmental authorities themselves. Morgan Stanley Research is disseminated in Brazil by Morgan Stanley C.T.V.M. S.A.; in Japan by Morgan Stanley MUFG Securities Co., Ltd. and, for Commodities related

research reports only, Morgan Stanley Capital Group Japan Co., Ltd; in Hong Kong by Morgan Stanley Asia Limited (which accepts responsibility for its contents); in

Singapore by Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number

200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters

arising from, or in connection with, Morgan Stanley Research); in Australia to "wholesale clients" within the meaning of the Australian Corporations Act by Morgan Stanley

Australia Limited A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents; in Australia to "wholesale

clients" and "retail clients" within the meaning of the Australian Corporations Act by Morgan Stanley Smith Barney Australia Pty Ltd (A.B.N. 19 009 145 555, holder of

Australian financial services license No. 240813, which accepts responsibility for its contents; in Korea by Morgan Stanley & Co International plc, Seoul Branch; in India by

Morgan Stanley India Company Private Limited; in Indonesia by PT Morgan Stanley Asia Indonesia; in Canada by Morgan Stanley Canada Limited, which has approved of

and takes responsibility for its contents in Canada; in Germany by Morgan Stanley Bank AG, Frankfurt am Main and Morgan Stanley Private Wealth Management Limited,

Niederlassung Deutschland, regulated by Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin); in Spain by Morgan Stanley, S.V., S.A., a Morgan Stanley group

company, which is supervised by the Spanish Securities Markets Commission (CNMV) and states that Morgan Stanley Research has been written and distributed in

accordance with the rules of conduct applicable to financial research as established under Spanish regulations; in the US by Morgan Stanley & Co. LLC, which accepts

responsibility for its contents. Morgan Stanley & Co. International plc, authorized and regulated by the Financial Services Authority, disseminates in the UK research that it

has prepared, and approves solely for the purposes of section 21 of the Financial Services and Markets Act 2000, research which has been prepared by any of its affiliates.

Morgan Stanley Private Wealth Management Limited, authorized and regulated by the Financial Services Authority, also disseminates Morgan Stanley Research in the UK.

Private UK investors should obtain the advice of their Morgan Stanley & Co. International plc or Morgan Stanley Private Wealth Management representative about the

investments concerned. RMB Morgan Stanley (Proprietary) Limited is a member of the JSE Limited and regulated by the Financial Services Board in South Africa. RMB

Morgan Stanley (Proprietary) Limited is a joint venture owned equally by Morgan Stanley International Holdings Inc. and RMB Investment Advisory (Proprietary) Limited,

which is wholly owned by FirstRand Limited. The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (DIFC Branch), regulated by the Dubai Financial Services

Authority (the DFSA), and is directed at Professional Clients only, as defined by the DFSA. The financial products or financial services to which this research relates will only

be made available to a customer who we are satisfied meets the regulatory criteria to be a Professional Client. The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (QFC Branch), regulated by the Qatar Financial Centre

Regulatory Authority (the QFCRA), and is directed at business customers and market counterparties only and is not intended for Retail Customers as defined by the

QFCRA. As required by the Capital Markets Board of Turkey, investment information, comments and recommendations stated here, are not within the scope of investment advisory

activity. Investment advisory service is provided in accordance with a contract of engagement on investment advisory concluded between brokerage houses, portfolio

management companies, non-deposit banks and clients. Comments and recommendations stated here rely on the individual opinions of the ones providing these

comments and recommendations. These opinions may not fit to your financial status, risk and return preferences. For this reason, to make an investment decision by relying

solely to this information stated here may not bring about outcomes that fit your expectations. The trademarks and service marks contained in Morgan Stanley Research are the property of their respective owners. Third-party data providers make no warranties or

representations relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damages relating to such data. The Global

Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and S&P. Morgan Stanley bases projections, opinions, forecasts and

trading strategies regarding the MSCI Country Index Series solely on public information. MSCI has not reviewed, approved or endorsed these projections, opinions,

forecasts and trading strategies. Morgan Stanley has no influence on or control over MSCI's index compilation decisions. Morgan Stanley Research or portions of it may not

be reprinted, sold or redistributed without the written consent of Morgan Stanley. Morgan Stanley research is disseminated and available primarily electronically, and, in

some cases, in printed form. Additional information on recommended securities/instruments is available on request. Morgan Stanley Research, or any portion thereof may not be reprinted, sold or redistributed without the written consent of Morgan Stanley. Morgan Stanley Research is disseminated and available primarily electronically, and, in some cases, in printed form. Additional information on recommended securities/instruments is available on request. M O R G A N S T A N L E Y R E S E A R C H The Americas Asia/Pacific United States United Kingdom Hong Kong Industry Coverage:Biotechnology Company (Ticker) Rating (as of) Price* (03/18/2013) David Friedman, M.D. AMAG Pharmaceuticals, Inc.

(AMAG.O) Alexion Pharmaceuticals (ALXN.O)

Sara Slifka Neurocrine Biosciences Inc

(OPTR.O) Marshall Urist, M.D., Ph.D. Amgen Inc. (AMGN.O)

Stock Ratings are subject to change. Please see latest research for each company. * Historical prices are not split adjusted.

Instructions: After reading through each section of the manual, complete this quiz. If you have difficulties, review the section one more time and attempt the quiz again. This process should be repeated until you have the correct answers for all of the questions. Directions: Fill in the blanks with the name of the correct body part. Choose from those that are listed below. 1. The ______________

Corporate Sector The corporate sector has witnessed robust financial performance during the half year ended (April-September) 2006-07, despite higher input costs impinging on profit margins. The increase in raw material cost has been much higher than all other components of operating and non-operating expenses during April-September 2006-07. Rising input costs such as raw material, power a

M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H  M O R G A N S T A N L E Y R E S E A R C H

M O R G A N S T A N L E Y R E S E A R C H